Deciding whether to rent or buy a home is one of the biggest financial decisions many Canadians face. The “rent vs. buy” debate isn’t just about money—it’s also about lifestyle, goals, and personal preferences.

In this post, we’ll break down the numbers, explore the advantages and disadvantages of each option, and provide a detailed example tailored to the Canadian context. Let’s dive in!

Table of Contents

At its core, the rent vs. buy decision compares the cost of renting a home with the cost of owning one. But there’s more to it than just monthly payments. Factors like home appreciation, rent increases, investment opportunities, maintenance, and property taxes all play a role. Here’s how they stack up.

Understanding the Financial Commitment

First, let’s take a closer look at the financial commitments of both options.

Renting typically requires a smaller upfront cost. You’ll likely need a security deposit and the first month’s rent. The good news is that you won’t be responsible for maintenance, repairs, or property taxes. Nevertheless, your rent may increase over time, and you’re building no equity.

Buying, on the other hand, involves a hefty upfront payment, which includes a down payment (usually between 5% and 20% of the home’s value), closing costs, and various fees. Homeownership also brings ongoing costs like property taxes, maintenance, and insurance. However, with each mortgage payment, you’re building equity in your home—a big financial benefit in the long run.

What Are Your Long-Term Plans?

One of the first questions to ask yourself when deciding to rent or buy is how long you plan to stay in one place.

Short-Term Stays: If you’re planning to live somewhere for less than five years, renting is likely the smarter choice. Moving within a few years of purchasing a home might mean you won’t recover your closing costs and other expenses.

Long-Term Commitment: If you plan to stay in one place for several years or more, buying might make more sense. Over time, the value of your home could increase, and you’ll have the chance to build equity.

The Flexibility Factor

Another important consideration is your lifestyle. Renting offers more flexibility, making it easier to move if your job changes or if you want to relocate.

Renting: Flexibility is one of the top reasons people choose to rent. You can move when your lease is up, making it an excellent choice for those who prefer not to be tied down. Whether it’s for a new job, relationship, or just a change of scenery, renting allows you to move without the burden of selling a property.

Buying: When you own a home, moving becomes more complicated. Selling a home can take time and often involves realtor fees and other costs. If you value the flexibility to pack up and move easily, renting may be the better option.

Maintenance and Responsibility

Maintenance and repairs are a key difference between renting and owning a home.

Renting: One of the biggest advantages of renting is that the landlord is typically responsible for repairs and maintenance. If the heater breaks or the roof leaks, you don’t have to worry about shelling out thousands of dollars for repairs.

Buying: As a homeowner, you’re responsible for any repairs that pop up. You’ll need to budget for ongoing maintenance costs like fixing appliances, landscaping, and keeping the property in good shape. This can be a significant expense, so be prepared to set aside money for unexpected repairs.

Building Equity

Building equity is one of the primary financial advantages of homeownership. When you make mortgage payments, a portion of that money goes towards paying down your loan balance, which increases your equity in the home.

Renting: When you rent, you’re paying for the right to live in a property, but you’re not building any financial ownership in it. Your monthly rent payments don’t contribute to long-term wealth, which is one downside of renting over buying.

Buying: With each mortgage payment, you build equity in your home. Over time, as the value of the home increases, so does your equity. This can be a key factor in long-term wealth-building.

What’s the Market Like?

The real estate market plays a crucial role in the buy vs. rent decision. If housing prices are high and expected to drop, renting might make more sense in the short term. Alternatively, if you’re in an area where home prices are relatively low and expected to rise, buying could be a smart investment.

Renting: In some markets, rental prices might be lower than the cost of a mortgage. In these cases, renting may allow you to save money in the short term and invest it elsewhere.

Buying: In other markets, buying may actually be cheaper than renting. If mortgage rates are low and home prices are affordable, buying could be a better option financially.

Related content:

Consider Tax Benefits

In Canada, both renting and homeownership come with unique tax considerations, but the benefits differ significantly.

Renting: Can You Claim Rent?

Yes, renters in certain provinces can claim rent on their taxes if they meet specific criteria. For example in Ontario, renters can apply for the Ontario Trillium Benefit (OTB), which includes the Ontario Energy and Property Tax Credit. To qualify, you’ll need a valid rental agreement and details about the rent paid.

While rent isn’t directly tax-deductible federally, provincial programs can provide some relief. Always check your province’s tax credits to see what you might qualify for.

Buying: Can Homeowners Claim Anything?

In Canada, tax benefits for homeowners are more limited than in some countries, such as the U.S. Here’s what to know:

- No Mortgage Interest Deduction: Unlike the U.S., Canadians cannot deduct mortgage interest or property taxes on their annual income taxes.

- Home Buyers’ Amount: First-time homebuyers can claim up to $5,000 on their taxes for the purchase of a qualifying home, resulting in a non-refundable tax credit of up to $750.

- Home Accessibility Tax Credit (HATC): If you make eligible renovations to improve accessibility for a person with disabilities or a senior, you may qualify for this credit.

- GST/HST New Housing Rebate: If you buy a newly constructed home, you might be eligible for a rebate on part of the GST or HST paid.

If you’re curious about the tax benefits of homeownership, the TurboTax app can help you estimate how much you’ll save. It breaks down your potential deductions and guides you through the tax implications of buying a home.

What’s Your Credit Score?

Your credit score plays a major role in both renting and buying. It can determine whether you’ll be approved for a mortgage or rental application, and it also affects the interest rate you’ll get on a loan.

Renting: A good credit score makes it easier to secure a rental. Some landlords may require a minimum score or charge higher security deposits for those with lower scores.

Buying: If you’re buying a home, your credit score will impact the mortgage interest rate you qualify for. A higher score can save you thousands of dollars over the life of your loan.

Use the Credit Karma app to monitor your credit score for free and get personalized tips on how to improve it. It’s a great way to ensure your credit is in good shape whether you’re renting or buying.

Related content:

- How Bad is a 560 Credit Score and How to Improve?

- A 760 Credit Score: Good Enough? 7 Proven Tips to Boost It

Do You Have a Down Payment and Are You Financially Prepared?

One of the biggest challenges of homeownership is saving for a down payment. Many lenders require a down payment of 20% of the home’s purchase price, although some offer options with lower down payments if you purchase mortgage insurance.

Beyond the initial payment, having a steady income is crucial for managing the ongoing costs of homeownership, such as mortgage payments, property taxes, and maintenance. Ask yourself: Are you financially prepared to handle these responsibilities?

Buying: Coming up with a down payment can be a significant hurdle for many. Yet, there are programs available for first-time homebuyers, such as down payment assistance or lower requirements, that can make homeownership more accessible.

Renting: Renting typically requires a much smaller upfront cost. A security deposit and the first month’s rent are usually all you need, making it a more affordable option upfront.

The Emotional Aspect

Finally, there’s the emotional component.

Owning a home is often seen as a cornerstone of the “Canadian Dream,” symbolizing pride, accomplishment, and stability. However, emotions also play a significant role when deciding between renting and buying.

Buying: Homeownership provides a deep sense of stability and belonging. It eliminates concerns about sudden rent increases or unexpected moves due to a landlord’s decisions. That said, it also ties you to a property, both emotionally and financially, until you sell it or pay off your mortgage.

Renting: Renting offers flexibility, which can feel liberating for those who value mobility and the lack of long-term financial commitment. On the flip side, the impermanence of renting—such as facing potential evictions or restrictions on personalizing your space—can leave some feeling unsettled or constrained.

The Math Behind Rent vs. Buy Calculator

Rent vs. buy calculators apply time value of money principles—like compound interest and future value—while adjusting for factors such as rent increases, home appreciation, and investment returns. Let’s crunch the numbers to compare renting and buying over five years.

Cost of Renting

Renting costs include:

- Monthly rent payments.

- Annual rent increases.

- Potential investment returns if savings (like a down payment) are invested.

Where:

- R: Monthly rent.

- i: Annual rent increase rate.

- N: Number of years renting.

- r: Annual investment return on savings.

Cost of Buying

Buying costs include:

- Mortgage payments.

- Property taxes.

- Maintenance or association fees.

- Home appreciation and equity buildup over time.

Where:

- M: Monthly mortgage payment.

- T: Monthly property taxes.

- Ma: Monthly maintenance costs.

- g: Annual home appreciation rate.

Comparing the Costs

To decide: Net Cost=Rent Cost−Buy Cost

- A positive result favors renting.

- A negative result favors buying.

Example: Renting vs. Buying over a 5 year period

Renting:

- Monthly rent: $2,200 (Canada national average for a two-bedroom apartment).

- Annual rent increase: 2.5% (applicable under rent control).

- Investment return on savings: 7.59% (S&P 500 real (inflation-adjusted) return over a 100-year period).

Buying:

- Home price: $729,000 (Canadian average).

- Down payment: $145,800 (20%).

- Mortgage rate: 4.5%.

- Loan term: 25 years.

- Property tax: 1% of home value annually.

- Maintenance cost: 0.5% of home value annually.

- Home appreciation: 3.28% annually (residential property prices in Canada have averaged an annual increase of 7.19% from 1971 to 2024, while the average annual inflation rate during the same period was 3.91%).

Step 1: Calculate Rent Cost

- Year 1 Rent: $2,200 × 12 = $26,400

- Rent increases by 2.5% annually:

- Year 2: $26,400 × (1 + 0.025) = $27,060

- Year 3: $27,736.50

- Year 4: $28,429.91

- Year 5: $29,140.66

- Total Rent Over 5 Years: $138,767.07

- Savings Investment: If $145,800 is invested at a 7.59% annual return for 5 years:

- FV = 145,800 × (1+0.0759)^5 = 210,192.43

Net Rent Cost: 210,192.43 − 138,767.07 = 71,425.36 (gain from investing savings)

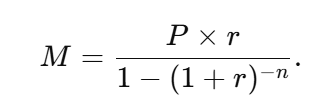

Step 2: Calculate Buy Cost

Mortgage Payment:

Using the formula for fixed monthly payments:

Where:

- Loan amount (P) = $583,200.

- Monthly interest rate (r) = 4.5% ÷ 12 = 0.00375.

- Total payments (n) = 25 × 12 = 300.

M = $3,227.85

Mortgage payments over 5 years: 3,227.85 × 12 × 5 = $193,671.00.

Other Costs:

- Property Taxes: 729,000 × 0.01 × 5 = $36,450

- Maintenance Costs: 729,000 × 0.005 × 5 = $18,225

Home Value After 5 Years: FV = 729,000 × (1+0.0328)^5 = $856,660.37

Equity Buildup: 856,660.37 − 512,028.53 (remaining loan after 5 years) = $344,631.84.

Net Buy Cost: 344,631.84 – (193,671.00 + 36,450 + 18,225) = $96,285.83 (gain from buying)

Step 3: Compare Costs

- Renting: $71,425.36

- Buying: $96,285.83

- Result: In this scenario, buying leads to a net “gain” of $24,860.47 over 5 years.

Tools to Help You Decide

There are several online tools to help personalize your rent vs. buy decision:

- The Rent vs. Buy Calculator from WOWA.CA compares the total cost of renting versus buying, factoring in home price appreciation, rental increases, and your financial situation to give you a clear picture of the best option.

- If you’re uncertain about your long-term plans, the CMHC Affordability Calculator can help determine how much home you can afford.

- To estimate how quickly you’ll build equity, use the Mortgage Calculator from the Canada Government. It lets you input your loan details to see how much equity you can accumulate over time.

- Apps like HouseSigma.com and Realtor.com offer real-time data on home prices, market trends, and how long homes are staying on the market, helping you stay informed about price fluctuations in your area.

You may also want to consider speaking with a financial advisor or mortgage specialist to better understand your financial readiness, if needed.

Final Thoughts: Rent or Buy?

The decision to rent or buy depends on your financial health, long-term plans, and personal priorities. Renting offers flexibility and lower upfront costs, making it ideal for those who prefer mobility or aren’t ready for the financial commitment of homeownership. In contrast, buying a home provides stability and the potential for long-term wealth-building, but it requires a larger initial investment and ongoing responsibilities.

By evaluating your financial situation and future goals, you can choose the option that best suits your needs. The key is to avoid overstretching yourself into a risky financial situation.

What’s your take on the rent vs. buy debate? Let us know in the comments below!